The 2025 Inexpensive Care Act (ACA) open enrollment interval has been a tough one, as Market enrollees are going through important premium hikes for 2026 protection. When Market protection—which has to fulfill ACA requirements for advantages, non-discrimination, and community adequacy—turns into more durable to afford, non-ACA compliant merchandise (generally known as “junk plans” due to the shortage of state and federal protections) could acquire traction, particularly when they’re marketed as low-cost alternate options to the Market and the federal authorities has relaxed enforcement.

These non-ACA compliant merchandise will be dangerous in 3 ways: as a result of they don’t seem to be topic to most state and federal medical insurance requirements, they usually include main protection limitations, together with skimpy advantages and an array of exclusions; these merchandise are sometimes misleadingly marketed as alternate options to ACA Market protection however the merchandise being bought should not main medical protection in any respect, making a false and complicated comparability; and these non-ACA merchandise are sometimes marketed towards comparatively wholesome people, siphoning off these populations from the person market and exacerbating the affordability points in that market.

State coverage makers can curb the supply of those merchandise or put guardrails and protections round them by means of laws or regulation. Within the fast time period, although, state insurance coverage regulators can ramp up oversight of those non-ACA compliant merchandise and extra aggressively monitor misleading advertising practices. Because the advertising of non-ACA compliant merchandise grows, shoppers who find yourself in a plan that was “too good to be true” can face important monetary hurt.

What Are “Junk Plans”?

Join our Free E-newsletter

By registering, I settle for the privateness coverage.

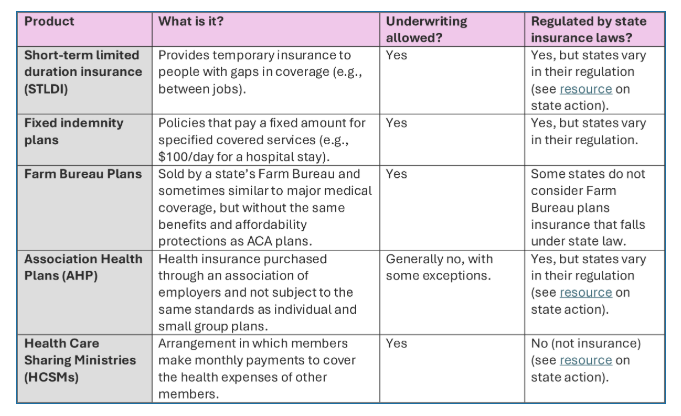

The time period “junk plans” is a catch-all meant to seize a variety of merchandise that don’t have to adjust to ACA protections akin to advantages necessities and non-discrimination provisions. Many of those merchandise deploy medical underwriting, which permits insurers to base the supply and value of a plan on a person’s well being standing. This could make these merchandise extra engaging to youthful folks with out preexisting situations. Exhibit 1 lists sorts of junk plans.

Exhibit 1: Sorts Of Junk Plans

Supply: Authors’ creation.

How Does Deceptive Advertising and marketing Of Junk Plans Influence Shoppers?

Most of the non-ACA-regulated merchandise described above should not meant to switch main medical insurance coverage. A set indemnity plan, for example, offers what is actually an revenue alternative profit when somebody is hospitalized, which might function an additional layer of monetary safety when paired with a significant medical insurance coverage plan. The issue arises when these non-ACA regulated merchandise are marketed as alternate options to main medical insurance coverage. Propping up a substandard product as simply one other insurance coverage plan alternative in a dizzying array of choices creates an apples to oranges comparability, with shoppers considering they’ve discovered an affordable different that finally ends up too good to be true.

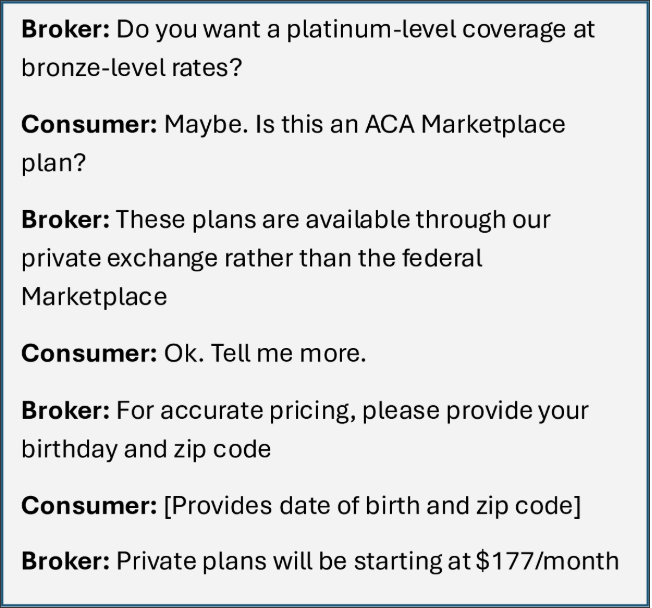

Take the instance from a dealer advertising textual content trade with one of many authors, described in exhibit 2.

Exhibit 2: Textual content trade with dealer

Supply: Authors’ transcript.

The implication is that the dealer is promoting a product on a “non-public trade” which may be an alternative choice to ACA Market protection (the Market can also be generally known as an trade, including, seemingly deliberately, to the confusion). Nonetheless, a name with this dealer revealed that the merchandise obtainable on this non-public trade are mounted indemnity plans. The dealer famous that in contrast to a Market plan, the non-public plan has no deductible or copayments, as a substitute it offers “first greenback protection” (which means the insurer begins fee as quickly as an insurable occasion happens with out requiring a affected person to fulfill a deductible or pay out of pocket on the level of sale) and is accessible at a premium a whole lot of {dollars} decrease than Market plans. Whereas it’s true {that a} mounted indemnity plan usually doesn’t include copayments or deductibles, this isn’t as a result of a client has discovered the deal of a lifetime. It’s as a result of the product will not be designed like an insurance coverage plan in any respect. With a set indemnity plan, shoppers could pay nothing after they obtain care, solely to be saddled with a invoice later after they study the plan’s mounted greenback fee for the service obtained doesn’t come near protecting the complete value, leaving the buyer answerable for the steadiness.

A number of research have documented deceptive advertising getting used to lure shoppers purchasing for protection into non-ACA regulated merchandise. A 2019 Georgetown CHIR examine discovered that short-term plans have been usually marketed as cheaper alternate options to “Obamacare” plans, leaving shoppers confused as to how short-term plans have been totally different from Market plans. An analogous 2020 evaluation from the Brookings Establishment and one other from CHIR discovered that deceptive advertising could have been much more pronounced throughout the COVID-19 pandemic as uninsured shoppers struggled to seek out protection choices amid widespread unemployment. A Authorities Accounting Workplace examine printed in 2020 carried out covert testing of selling practices for choose non-ACA compliant merchandise and located that in 1 / 4 of their covert calls “gross sales representatives engaged in doubtlessly misleading advertising practices … by omitting or misrepresenting details about the merchandise they have been promoting.” Extra lately, CHIR researchers discovered brokers utilizing deceptive advertising to steer low-income shoppers dropping Medicaid to restricted profit plans.

What Are State Regulators Doing About Junk Plans?

Whereas deceptive advertising of non-ACA compliant plans will not be new, it might be a extra pronounced downside throughout an open enrollment interval when shoppers are going through giant Market premium hikes. There are two routes that states can take to guard shoppers, and their insurance coverage markets, from the harms related to most of these merchandise. First, states can place guardrails across the merchandise themselves, in some instances prohibiting their sale altogether or placing situations on their sale.

Second, states can tamp down on deceptive advertising of non-ACA compliant merchandise. State insurance coverage regulators have major authority over the regulation of insurance coverage, together with licensure and oversight of insurance coverage brokers. Some states require particular client “black field” warnings on these merchandise, requiring carriers to disclose clearly that the product will not be compliant with the ACA and in some instances how the product differs from ACA protection. State insurance coverage departments—together with Colorado, Maryland, and Texas—have issued steering for shoppers on easy methods to inform Market protection from non-ACA compliant merchandise. New Mexico issued steering placing insurers and brokers on discover that misleading and deceptive advertising is illegitimate beneath state client safety legal guidelines.

Not all non-ACA-compliant plans are inherently dangerous to shoppers, however when they’re marketed as low-cost alternate options to main medical protection, shoppers can discover themselves enrolled in merchandise that don’t really present the monetary safety they thought they have been getting. The Trump administration is transferring ahead with a proposed regulatory agenda that features increasing entry to non-ACA compliant merchandise and even incentivizing states to decontrol these plans. States, nonetheless, have an excessive amount of regulatory authority over many of those merchandise, as a new report from Blood Most cancers United factors out. States could think about implementing extra guardrails and heightened oversight to make sure shoppers don’t find yourself underinsured or in substandard merchandise they thought have been main medical plans.

Amy Killelea and JoAnn Volk “The Peddling Of “Junk Plans” To Shoppers Going through Larger Insurance coverage Premiums” January sixteenth, 2026, https://www.healthaffairs.org/content material/forefront/peddling-junk-plans-consumers-facing-higher-insurance-premiums. Copyright © 2026 Well being Affairs by Venture HOPE – The Folks-to-Folks Well being Basis, Inc.