Preliminary information present insurance coverage corporations have paid out greater than $4 billion for losses from the most important two of the Los Angeles-area wildfires that swept by way of the area and destroyed tens of 1000’s of properties earlier this month.

This week the image of simply how damaging the L.A. wildfires have been is coming into focus now that claims professionals have been in a position to acquire some entry to the affected areas.

Claims figures from insurers launched by the California Division of Insurance coverage on Jan. 30 present that 31,210 claims have been filed for house, enterprise, residing bills and different disaster-related wants. In keeping with CDI, $4.2 billion in claims have been paid.

The figures, that are for the Palisades and Eaton fires, are prone to rise. At this level they give the impression of being to be heading up towards early estimates from modelers which have come out in current weeks pegging insured losses at between $8 billion and $40 billion.

State Farm, the state’s high owners insurer, this week stated it has paid practically 10,000 claims value roughly $500 million from house and auto injury.

“As of Tuesday (Jan. 28), we’ve acquired over 10,200 complete house and auto claims and have already put effectively over a half a billion {dollars} again into clients’ palms,” a press release from State Farm reads. “We anticipate these numbers will proceed to rise as residents return and assess injury. We are going to proceed to course of claims for our clients. We’ve made profitable voice-to-voice contact with over 95% of consumers who’ve filed owners claims.”

In keeping with a State Farm spokesman, many of the owners claims are for fireplace or smoke injury to property and sometimes contain a declare for extra residing bills.

In L.A. County, State Farm studies insuring 250,000 properties and 880,000 vehicles.

Insurer Chubb this week stated the wildfires will price the insurer $1.5 billion within the first quarter. The service’s anticipated payouts have been revealed in a monetary assertion that detailed the corporate’s fourth-quarter 2024 outcomes.

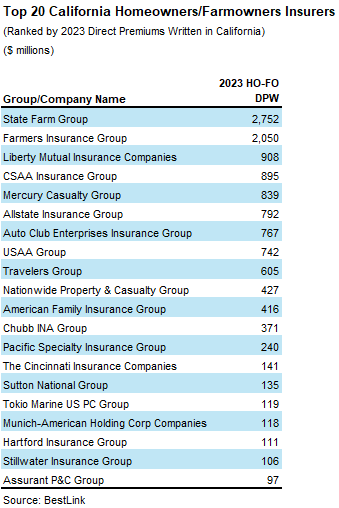

Different carriers have but to report on insured losses. Following State Farm, the state’s largest owners insurers are Farmers Insurance coverage Group, Liberty Mutual Insurance coverage Corporations, CSAA Insurance coverage Group, Mercury Insurance coverage Group, Allstate Insurance coverage Group, Auto Membership Enterprises, USAA Group and Vacationers Group, in keeping with AM Finest’s newest information.

Whereas claims professionals are entering into many areas, mop up and security concerns proceed to hamper full entry, in keeping with Mark Sektnan, vp of the American Property Casualty Insurance coverage Affiliation (APCIA).

Sektnan stated he expects the figures on insured losses to proceed rise.

“Definitely, I’d assume they might go up,” he stated. “Some corporations could also be paying out on property claims, or on further residing bills – corporations are following the regulation that requires them to pay explicit percentages for protection and supply further residing bills for a sure period of time. And so sure, the claims will certainly go up as we get farther into the rebuilding course of.”

The FAIR Plan reported that as of Jan. 28 it has acquired greater than 3,200 claims for injury attributable to the Pacific Palisades Hearth and greater than 1,200 claims for injury attributable to the Eaton Hearth.

A number of claims developments value noting are already rising from the wildfires. One is that many properties affected by the fires have been completely destroyed by the blazes, which blew up within the interval of a few day, pushed quickly over brush by hurricane-force winds.

There isn’t a lot left of many properties, that are being declared complete losses, in keeping with one claims specialist.

“We’re seeing complete losses,” stated Thomas Carstens, vp, U.S. property/casualty for Crawford. “We’re going on the market and there’s actually nothing to see. We’re perhaps measuring the perimeter of a constructing attempting to determine just a little bit what the construction seemed like, if there’s any private property left, that form of factor.”

He stated claims professionals he has spoken with are taking all losses into consideration, however the course of has change into considerably fundamental as a result of there are fewer partial losses. They’re utilizing estimating platforms to determine a substitute price and further money worth, and are contemplating every other coverages on the property, in addition to estimating inventories for private property, coverages for particles elimination, and advance funds for extra residing bills.

However with so many complete losses, there’s not a lot else to do.

“Many of those claims are being settled based mostly on a a lot quicker strategy, using square-foot kind valuations…as a result of the character of the fires have been so damaging,” he stated.

Carstens has seen one other pattern rising: properties, notably the multi-million-dollar properties, are too usually turning out to be underinsured.

“The values of those properties are excessive and that’s one other characteristic…a few of these areas didn’t have insurance coverage to 100% of worth,” Carsten stated. “Some individuals are insured to complete worth of the chance, however a few of them have an insurance coverage restrict that’s lower than the substitute price.”

This can be a part of the fallout from the state’s owners insurance coverage affordability and availability disaster. It seems some owners, particularly these with high-value properties or these in risker areas, started accepting extra threat because the phrases of protection grew to become harsher.

As charges and availably worsened in recent times on the again of extra frequent and longer wildfire seasons, brokers centered on high-net-worth people, and properties started reporting more durable experiences with carriers when attempting to safe protection on multi-million properties. Some brokers have been extra usually seeing limits of half the whole worth of properties, excessive wildfire deductible, and a whole lot of 1000’s of {dollars} in premiums.

Extreme wildfire seasons made insurers cautious. CalFire information present that seven of the state’s 10 most damaging wildfires have occurred within the final 10 years. Carriers started pulling again from the state’s owners market, blaming wildfire losses in addition to rules. In addition they started requesting steep charge will increase.

State Farm utilized for big charge will increase in California, a yr after the service bought charge approvals of seven% and 20%. The service insures practically one-in-five properties within the state. It extra not too long ago requested a 30% charge enhance for its owners line, a 52% charge enhance for renters and 36% charge enhance for rental protection.

Allstate, which stopped issuing new California owners insurance coverage insurance policies in 2022, sought a rise in its California owners insurance coverage premiums by a median of 34%.

In response, California Insurance coverage Commissioner Ricardo Lara launched his so-called Sustainable Insurance coverage Technique to extend protection in wildfire-distressed areas of the state. Lara in December introduced a disaster modeling and ratemaking regulation that may enable carriers to make use of the fashions as a think about setting and getting charges.

The modifications to the rules have been effectively acquired by the insurance coverage trade, however they could do little to right away sooth the affect from the L.A. fires, that are anticipated to trigger property insurance coverage carriers to boost charges, cut back protection choices, or each, in California and different at-risk areas, in keeping with S&P.

“California wildfires have had a major affect on the U.S. property insurance coverage trade over the previous three a long time, driving up premiums, shaping underwriting practices, and difficult regulatory reform,” S&P said. “The latest California wildfires, which began in early January in Los Angeles County, are anticipated to end in substantial losses for insurers. Put up occasion, we imagine property insurance coverage carriers will increase charges and/or cut back protection choices.”

Preliminary estimates from Moody’s RMS are for insured property losses to be as a lot as $30 billion from the fires. Disaster modeler KCC stated insured loss from privately insured and California FAIR plan insurance policies to residential, business and industrial properties, and autos from the Palisades and Eaton Fires will probably be near $28 billion.

Estimates issued by Verisk peg insured losses to property from the Palisades and Eaton fires between $28 billion and $35 billion, which incorporates losses to the California FAIR Plan.

The very best figures issued on insured losses up to now embrace a excessive of $40 billion put out final week from Keefe Bruyette & Woods analysts. CoreLogic indicated a $35 to $45 billion vary of insured losses for 2 main fires in Los Angeles.

At one level the L.A. space had 5 important ongoing wildfires. Complete losses from the fires are anticipated to be huge. AccuWeather revised its preliminary estimate of the whole injury and financial loss from the fires to between $250 billion and $275 billion.

The CDI figures, launched beneath an initiative from Lara, the public client claims monitoring system, additionally present 14,417 claims partially paid beneath legal guidelines requiring advance funds to hurry restoration. Lara issued a bulletin on Jan. 23 ordering insurers to offer advance funds for changing private property or contents in an quantity that’s 30% of the coverage’s dwelling restrict, as much as $250,000, with out requiring policyholders to file an itemized declare, and an advance fee of a minimum of 4 months of residing bills.

The majority of unpaid claims embrace property injury and particles elimination, which will probably be paid when folks start the method of rebuilding and particles elimination, in keeping with the CDI.

“With a lot misinformation and hypothesis about our insurance coverage market after the Southern California wildfires, it’s crucial for the general public to trace claims and monitor payouts,” Lara stated in a press release. “All eyes are on the insurance coverage corporations, and so are mine. I would like shoppers to know that we’re intently monitoring all the claims course of to make sure they’re protected. I anticipate insurance coverage corporations, together with the FAIR Plan, to proceed offering advance funds which might be important for getting survivors again on their toes as rapidly as doable.”

Subjects

Disaster

Pure Disasters

Wildfire

Louisiana