A brand new report from the Authorities Accountability Workplace finds that common premium will increase between threat ranges are bigger for wind than for wildfire.

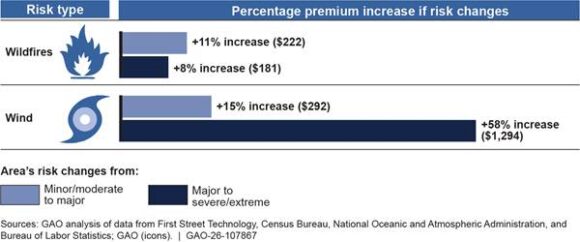

Between 2019 and 2024, properties in areas categorised as extreme or excessive wind threat had premiums about 58% increased on common—roughly $1,294 extra per yr—than related properties in main wind threat areas, the following decrease class.

By comparability, premiums for properties in extreme or excessive wildfire threat areas had been about 8% increased—roughly $181 extra yearly—than these in main wildfire threat areas.

The findings spotlight variations in how premiums differ throughout disaster threat classes, notably on the highest threat ranges. The report additionally exhibits a 15% premium enhance, or about $292 per yr, between minor/average and main wind threat areas. This compares with an 11% enhance, or roughly $222 per yr, for wildfire threat over the identical vary.

Premiums in areas at extreme or excessive threat for wind and wildfire additionally grew sooner than premiums in areas at main threat, the workplace reported.

“For instance, for annually since 2021, premiums in ZIP codes with extreme or excessive threat for wind or wildfire grew by 6–10% on common, and premiums for ZIP codes with main threat grew by 1–4%,” the report stated.

Associated: California Drought, Wildfire Dangers Develop as Snow Falls Brief

General, the GAO reported that U.S. householders premiums typically tracked inflation between 2019 and 2024 however rose extra in disaster-prone areas.

The common premium rose about 3% throughout that point after adjusting for inflation, whereas charges in elements of sure states, notably southern coastal areas at excessive threat of wind harm, rose by 25% or extra.

Many coastal areas of North Carolina and Texas noticed will increase of greater than 50% in actual phrases, the report stated. The best share will increase in estimated common premiums occurred in elements of North Carolina, Texas, Utah, Florida and California.

After being requested to evaluation points associated to householders insurance coverage, the GAO analyzed 2019–2024 knowledge on non-public householders protection and 2014–2023 knowledge on insurers of final resort to provide its tendencies report.

The workplace additionally interviewed representatives from the Federal Insurance coverage Workplace, 4 insurance coverage business teams, three shopper advocacy organizations and 4 state insurance coverage regulators.

Taken with Disaster?

Get automated alerts for this matter.